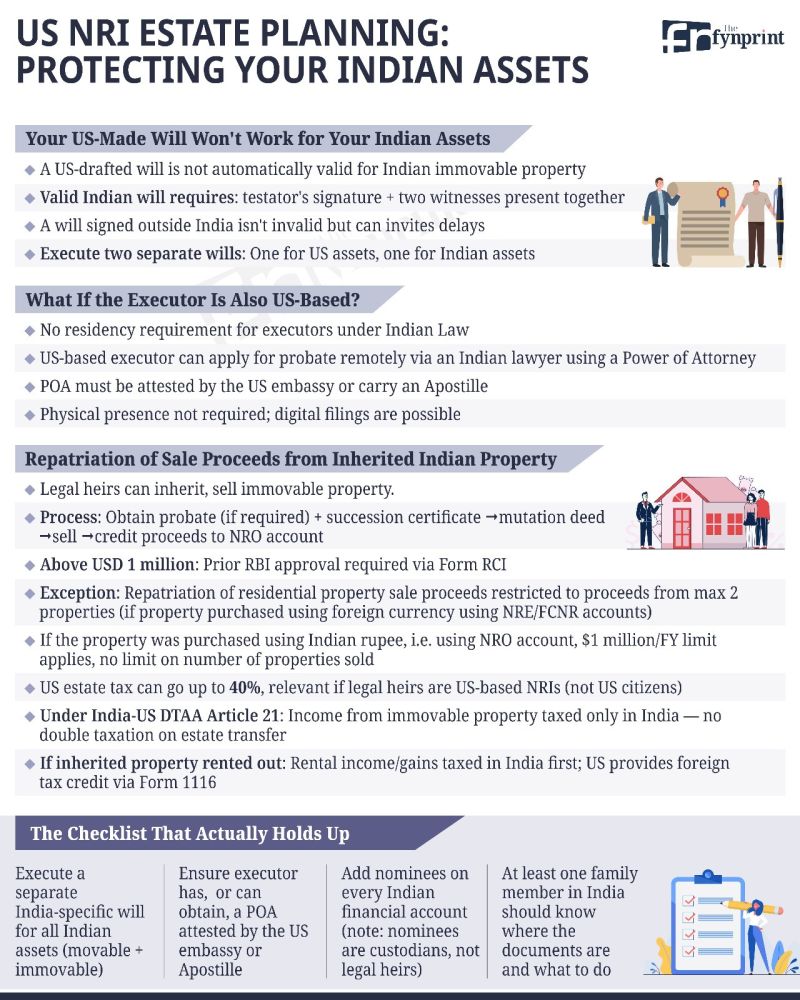

Most US-based NRIs think they have an inheritance plan for their Indian assets.

A US-made will. A nominee on the bank account. A family member in India who knows where the documents are.

Estate lawyers we spoke to say this plan almost never holds up.

Three things that trip families up most often:

1. A US-drafted will isn’t automatically valid in India. To work cleanly under Indian laws, it needs the right attestations, which is why lawyers recommend a separate India-executed will for Indian assets.

2. A nominee is a custodian, not a legal owner. Heirs can still need a succession certificate before banks release funds.

3. Repatriation isn’t a free pass. Up to $1 million per financial year is permitted post-sale, but the rules differ depending on whether the property was bought via NRE/FCNR or NRO accounts.

The fix isn’t complicated. But it has to be complete, and put in place before, not after.